What Reddit Taught Me About the Persistent Myths of Mortgage Shopping

Mortgage shopping sounds simple on the surface — get a rate, compare, pick the best one. In reality, it’s one of the most confusing financial processes borrowers go through, especially the first time. After spending months reading borrower discussions online, clear patterns emerge around what people misunderstand and where the process breaks down.

Quick Takeaways

- Mortgage rates are not tightly clustered — they vary widely across lenders

- Large, well-known lenders are not consistently the most competitive on pricing

- Getting 1–2 quotes is statistically likely to land you near the middle of the market

- Most benchmarks show averages — not the best rates actually available

Where the Confusion Starts

Spend time in mortgage-related discussions and the same questions come up repeatedly: “Is this a good rate?”, “Why is another lender quoting something so different?”, “Do I really need more than one or two quotes?” These aren’t random questions — they reflect a deeper issue. Borrowers are trying to make decisions without a clear view of how the market actually behaves.

Myth #1: All lenders should be close on rates

Many borrowers assume mortgage rates behave like an efficient market, where pricing clusters tightly around a single “fair” level. That assumption is understandable — borrowers see benchmarks and expect lenders to be similar.

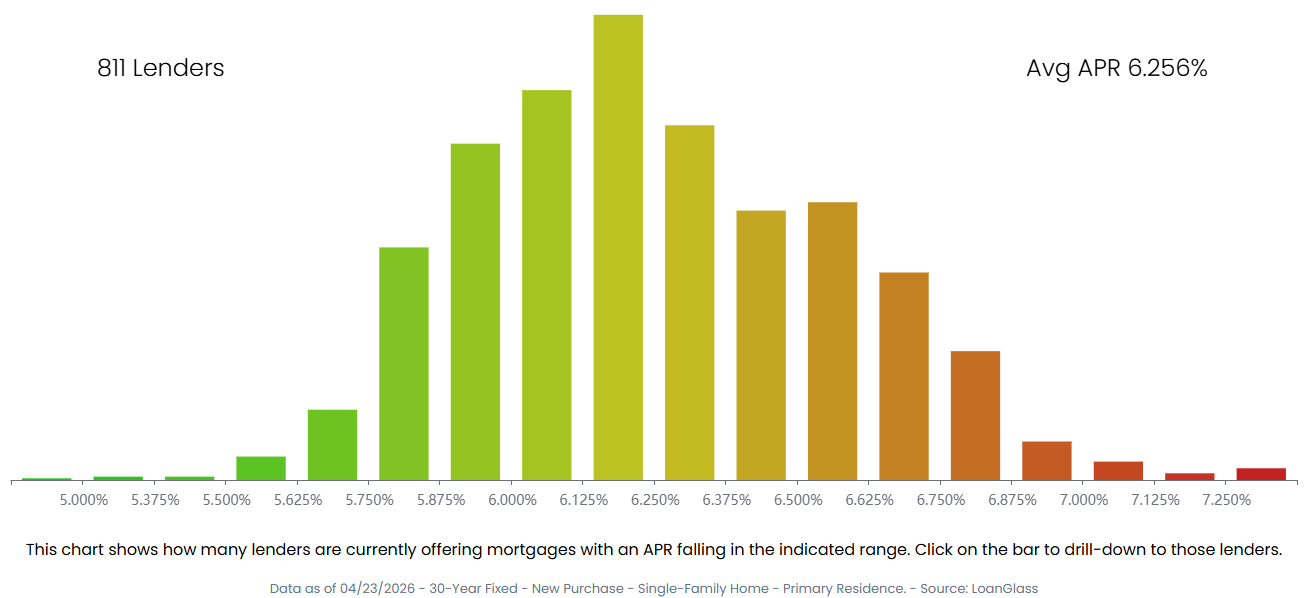

But mortgage pricing is not a tight cluster — it is a distribution. Rates are spread across a range, with a dense middle and meaningful differences between the median and the most competitive offers.

Two borrowers with similar profiles can receive significantly different quotes depending on which lenders they contact. The variation is not noise — it is structural.

The chart below illustrates this pattern, showing how many of the largest lenders consistently fall on the higher side of the rate distribution rather than at the most competitive edge.

Myth #2: Bigger lenders usually offer better rates

Borrowers often focus on a small set of large, well-known lenders. This feels logical — scale, brand recognition, and familiarity suggest efficiency and competitiveness.

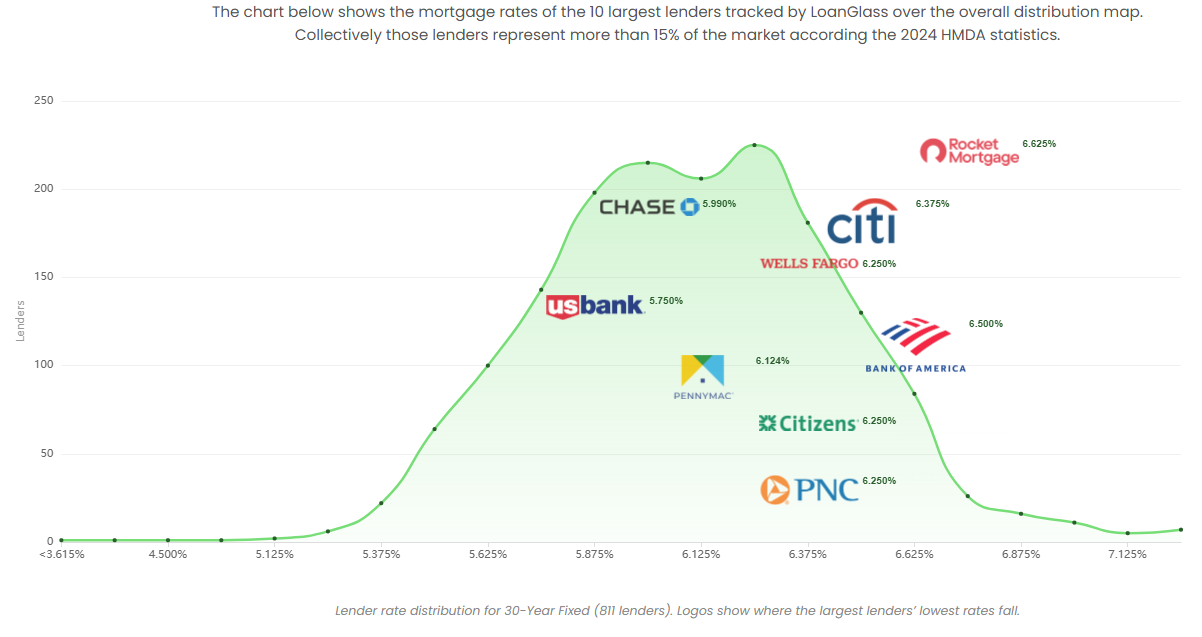

In practice, large lenders do not consistently sit at the most competitive end of the market. When mapped onto a distribution, many cluster closer to the middle — and sometimes higher.

This does not mean they are uncompetitive. They offer convenience, process efficiency, and strong customer experience. But brand size is not a reliable proxy for price competitiveness.

The chart below illustrates this dynamic, showing both how most lenders cluster around the middle of the distribution and how large lenders tend to appear on the higher side—making limited shopping even more likely to miss the most competitive offers.

Myth #3: One or two quotes is enough

Most borrowers stop after one or two quotes. The process is time-consuming, and each additional lender requires effort. But this approach creates two problems.

Problem 1: No clear baseline

Borrowers don’t know what a “good rate” looks like. Most available benchmarks represent averages — which sit near the middle of the market.

Benchmarks answer “what is typical,” but borrowers need to know “what is achievable.” Using averages does not help reach the most competitive end of the market.

Problem 2: Limited sampling leads to predictable outcomes

If a borrower contacts one or two lenders at random, they are statistically likely to land near the middle of the distribution — where most lenders sit.

Without a way to identify competitive lenders upfront, borrowers are effectively sampling blindly. In that scenario, overpaying is not bad luck — it is the expected outcome.

The Underlying Issue: Lack of Visibility

Across all of these patterns, the same root problem appears: borrowers do not have a clear view of the market.

They cannot easily see how wide the range of rates is, where a lender sits within that range, or what a truly competitive offer looks like.

A Shift Toward Transparency

Mortgage shopping does not need to be perfect to be significantly better. What borrowers need first is visibility — into how rates are distributed, where quotes fall, and what realistic options exist before engaging lenders.

At LoanGlass.com, mortgage pricing is tracked and normalized across hundreds of lenders in real time and presented as a distribution rather than a single number. This makes it possible to see not just where rates are on average, but where the most competitive offers actually sit in the market.

Final Thought

The questions borrowers ask are not random — they are signals. They point to a market where pricing exists, but is not easily visible in a way that supports decision-making.

Once that visibility improves, many of the myths around mortgage shopping begin to disappear on their own.

The mortgage rates displayed on this site are collected daily from publicly available sources provided by more than 800 lenders. LoanGlass does not receive compensation for listing these rates, and all rates are presented as published by the respective lenders. While every effort is made to ensure accuracy, the information may contain errors or omissions. Mortgage rates are highly dependent on an individual’s financial circumstances, credit profile, loan terms, and other factors. As such, the rates you are quoted directly by a lender may differ materially from the rates displayed here.

Users should contact lenders directly to obtain formal, binding loan offers. If you identify any discrepancies in the data or would like to have your institution’s rates included, please contact us at content@loanglass.com.

All logos, trademarks, and brand names appearing on this website are the property of their respective owners.

Help Us Help You

What would make LoanGlass more useful to you?

Thanks!

We appreciate your feedback.

About the author

LoanGlass